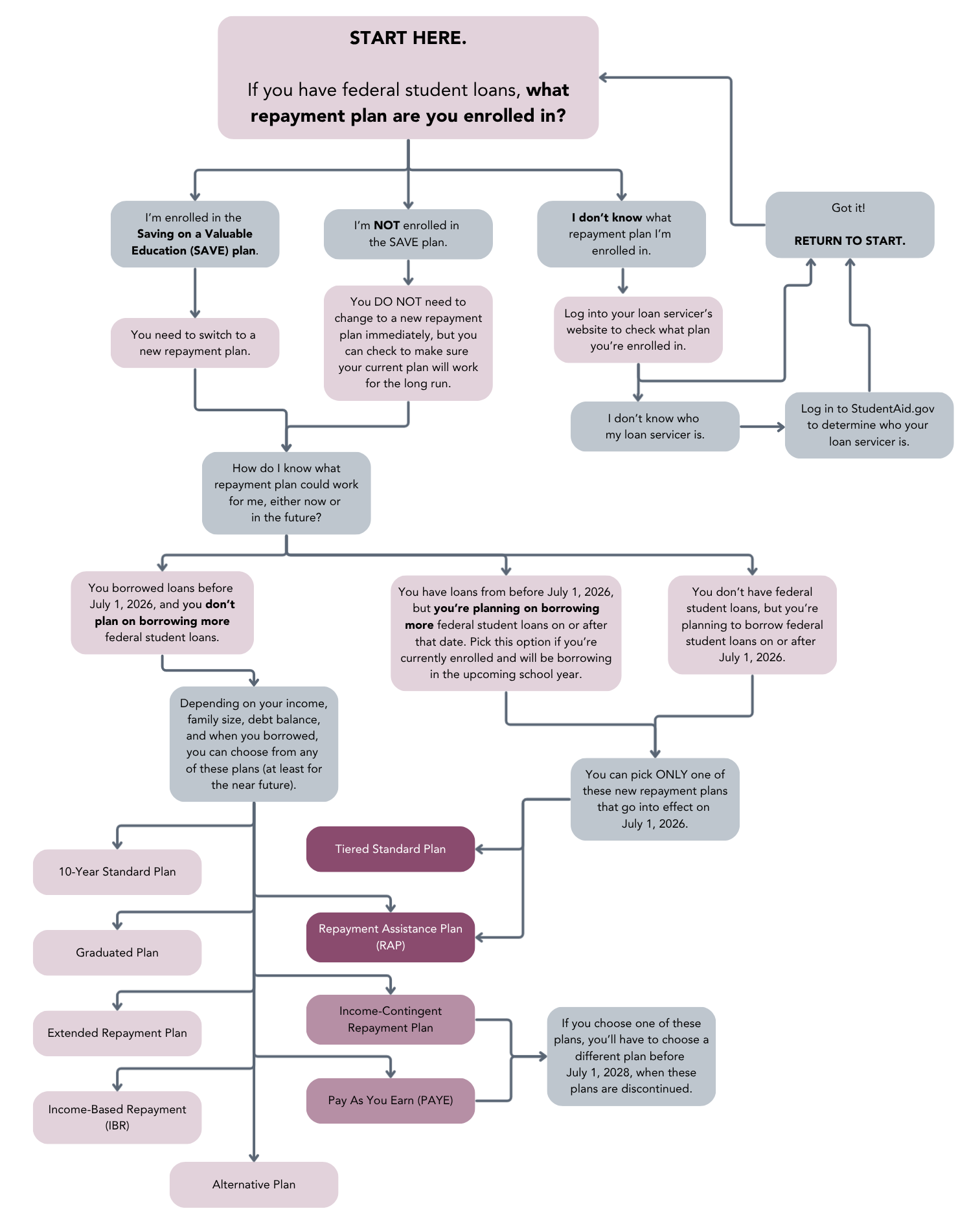

“In mere days, more than 35 million federal student loan borrowers in repayment will face a new set of choices when it comes to managing their debt. While these topics have received increasing coverage in the news media, the changes are sweeping and challenging to understand, even for those who have successfully navigated complex repayment options in the past. To make sense of the new options, borrowers first need to understand why the rules are changing and what those changes may mean for them. From there, the flow chart below can help borrowers think through their options and identify potential next steps. Why are things changing? Remember last year’s One Big Beautiful Bill Act (OBBBA)? Student loan borrowers will soon see its impacts in action. Two big policy revisions go into effect on July 1, 2026 that will affect borrowers in repayment on their federal student loans: Two new repayment plans created under OBBBA. The terms of a settlement reached from lawsuits filed by 18 Republican attorneys general against the Biden Administration’s Saving on a Valuable Education (SAVE) repayment plan. You may be wondering why the Trump administration’s plan gets to stand while Biden’s repayment plan is erased. It has to do with how each administration went about changing the law. While the new plans launching on July 1 were codified in the OBBBA legislation, the Biden administration modified regulations to create SAVE — meaning that the plan and its terms weren’t explicitly authorized under the law. While this method of creating new income-driven repayment (IDR) plans had succeeded in the past, SAVE was a much more generous plan, forgiving loans for some borrowers after as little as 10 years of payments. The lawsuit filed against SAVE claimed the plan went well beyond the boundaries set by existing federal law. After some legal back and forth , the Trump administration settled the suit and agreed to dismantle SAVE. As a result, the SAVE plan is no longer an option, but two new plans — the Tiered Standard plan and Repayment Assistance Plan (RAP) — are going into effect. Right now, almost 7 million borrowers are still enrolled in SAVE , even though a court-ordered injunction blocked it from taking effect nearly two years ago. This means that borrowers enrolled in SAVE haven’t made payments since at least July 1, 2024 — and due to the COVID payment pause, many of these borrowers have not made payments since March 2020, over six years ago. But things have slowly evolved. On Aug. 1, 2025, loans in SAVE started to accrue interest , and starting July 1, borrowers enrolled in SAVE will need to enroll in a different plan or risk being moved into one they didn’t choose. Even for borrowers not enrolled in the SAVE plan, it’s worth paying attention to these changes. While not everyone needs to take action now, some existing plans will sunset in two years, and borrowers taking out new loans will have entirely different options than in the past. If you’re not sure how these changes impact you, read on. What repayment plans can I choose? For borrowers who need, or want, to change their repayment plan, the options can be confusing as new plans become available and others are phased out. Use this flow chart to figure out what plans you can use to repay your loans. Figure: Charting Your Repayment Next Steps (Click to enlarge) Once you’ve determined what plans you’re eligible for, learn more about each plan in the interactive table below. Table: Important Details About Repayment Options Note : *For all income-driven repayment plans, your AGI is based on your tax filing status. If you are married filing jointly, your spouse’s income will be counted toward your AGI, but if you file separately, only your income will be counted in your AGI. Read this blog for more information. A few considerations : You have 90 days to enroll in a new plan. Loan servicers will start reaching out to borrowers in SAVE on July 1 to help them navigate their options. Borrowers will have 90 days from July 1 to enroll in a new plan, or they will be put into the Standard or Tiered Standard Plans. These plans will likely lead to significantly higher monthly payments, so your best bet is to choose a plan that fits your circumstances before the beginning of October. How to pick a plan. You can find more specific information about the terms of old and new plans on StudentAid.gov , including some of the more nuanced options . The best bet, though, is to log on to StudentAid.gov to estimate how much your monthly payments will be , since you may not be eligible for all plans based on when you borrowed and what type of loans you have. Keep in mind: the new plans aren’t in this tool yet, so make sure to log in after July 1 to assess all of your options. You can also check what repayment plan you’re in, when you borrowed each loan, and who your servicer is by logging into StudentAid.gov . You can apply for an IDR plan online, which is the most efficient way to get enrolled. To switch into other plans, you should check your account on your servicer’s website to see if there are online tools you can use, or you can call them. Don’t put off enrolling in a new plan for too long, as processing delays could occur due to an influx of new IDR applications. RAP: Higher payments, lower balances. While RAP will likely have many borrowers paying more per month than they did under older plans, RAP has a couple of provisions designed to curb a problem with older IDR plans, where borrowers’ outstanding interest balances could balloon if their payments weren’t able to cover the interest that accrued each month. Under RAP, if a borrower’s payment only goes toward interest, the remaining interest accrued in a given month that wasn’t covered by the payment is forgiven. In other words, if you accrued $100 in interest but your payment was $75, the remaining $25 in accrued interest would be removed from your balance sheet. And as an added bonus, if your payment doesn’t reduce your principal by more than $50, the U.S. Department of Education will contribute the difference — up to $50 — to ensure your principal is reduced by at least $50. So, for the borrower with the $100 payment described above, not only would they have the remaining $25 in interest removed from their account, but their principal balance would also be reduced by $50. However, if that borrower’s income changes and their payment jumps from $75 to $130, they would pay down their accrued interest and $30 of their principal, then the government would kick in an additional $20 toward their principal. This helps reduce interest accrual long term and ensures borrowers only see their balances go down, not up. The only caveat is that borrowers need to make full, on-time payments to qualify for these benefits; enrolling in auto-pay is the best way to ensure you don’t pay late or too little. Consolidation caution. When a borrower consolidates their existing federal student loans through the federal government, it creates a new loan. This consolidation loan has a new origination and disbursement date, which impacts what plans borrowers can access. At this point, borrowers should very carefully consider what they might lose in consolidating their debt — including access to older repayment plans that could offer more affordable payments, and credit already accrued toward IDR forgiveness. Consolidation may be most tempting — and potentially worthwhile — for borrowers with older loans borrowed through the Federal Family Education Loan Program (FFELP). If you’re not sure if you have FFELs, Federal Student Aid provides information on how to tell if you do and what you should consider before consolidating. Limited options for Parent PLUS borrowers. While Parent PLUS borrowers have always had a more limited set of repayment options, they’ll be even more constrained after July 1. If you have a Parent PLUS loan and haven’t already consolidated your debt into a new loan, you’ll lose access to all income-driven repayment plans — including RAP — as well as any path to loan forgiveness through IDR or PSLF. Borrowers with their own debt who have children approaching college age should also approach PLUS borrowing with caution, lest they lose access to more affordable repayment plans by taking on a new parent loan for their child. The best bet for Public Service Loan Forgiveness (PSLF) is an income-driven plan. Borrowers pursuing PSLF should note that the best bet for getting payments to count toward forgiveness is to enroll in one of the income-driven repayment plans (IBR, PAYE, ICR, or RAP). Why is this all so complicated? Although Congress touted that OBBBA would simplify repayment for borrowers, that’s really only the case for new borrowers as of July 1, 2026, who will have just two options — RAP and Tiered Standard. For other borrowers, the constantly shifting repayment environment has introduced complexity and compounded frustration, even as new options were designed to be more generous. One factor driving this complexity is the mechanism for change; Congress couldn’t legally make certain changes through the reconciliation process , leading to the forthcoming complexity. But it’s also worth noting that making policy through executive action rather than going through traditional legislative vehicles, such as reauthorization of the Higher Education Act, means ongoing volatility for borrowers as legal challenges wend their way through the courts. After all, this is what happened with broad-based debt forgiveness and the SAVE plan. At the end of the day, things will only get better for borrowers if Congress rolls up their sleeves, puts aside their differences, and gets to work making actual, bipartisan policy. Colleen Campbell is a senior associate partner at Bellwether and can be reached at colleen.campbell@bellwether.org . Previously, they served as the executive director of the Office of Loan Portfolio Management in the U.S. Department of Education’s office of Federal Student Aid, among many other roles throughout their tenure. The post Student loan repayment is changing. Here’s what you need to do. appeared first on Bellwether .

Original story

Continue reading at Bellwether

bellwether.org

Summary generated from the RSS feed of Bellwether. All article rights belong to the original publisher. Click through to read the full piece on bellwether.org.